Financial Intelligence

Mirror, Mirror, on the Wall—Is My Funding Strategy the Fairest of Them All?

by Frank L. Farone of Darling Consulting Group

As the current interest rate cycle progresses, the yield curve has inverted with long-term treasury rates testing historic lows. The push on deposit growth in 2018 has left many banks and credit unions with a higher cost of funds than in years past, while asset yields continue to plummet in 2019. The financial services industry in 2019 is in store for shrinking margins and ultimately lower levels of ROE, which suggests that institutions should consider developing a meaningful and cost-effective funding game plan to “muscle through” the current environment and help support growth requirements. Historically, most community institutions need to grow assets by 7-10% annually just to cover increased operating costs and maintain minimal acceptable returns on capital. High-performing institutions strategically incorporate a wholesale funding strategy to complement their retail/commercial deposit generating activities. It’s prime time to take a look in the mirror and challenge the appropriateness of your funding strategy(ies). Now is not necessarily the time to shrink wholesale funding levels, but rather to consider how wholesale funding might be able to support your earnings challenges in this historically low rate environment. In doing so, you may find that wholesale funding is a necessary and profitable risk management tool.

Why Are Institutions Reluctant to Use Wholesale Funding?

Common themes resonate with a sustained reluctance to use wholesale funding sources for anything other than temporary financing. Reasons for not using wholesale funding usually include one or more of the following:

Community institutions perceive wholesale funding to be costly. They would rather increase deposit rates than consider a lower-costing wholesale alternative.

A philosophy that deposits reflect customer relationships while borrowings do not, thus wholesale funding does little to increase the value of a franchise or attain the institution’s mission.

Perceived lack of spread, especially when financing securities with borrowings, thereby resulting in a lower return on assets.

Perceived negative regulatory attitude, which perpetuates board/management negativity.

Wholesale Funding Can Be the Cheapest Source of Funding

In lieu of borrowing money, some institutions continue to offer above-market rate, premium deposit specials in their local markets at rates significantly higher than wholesale! The true effective cost of any new money raised, as well as funds maintained, needs to be compared to the marginal cost of lowering rates across the board to see what sticks and what rolls out the door. The results will be a real eye opener, and the impact to bottom-line profits might be greater than you would have imagined — and potentially more profitable than most investment strategies you consider.

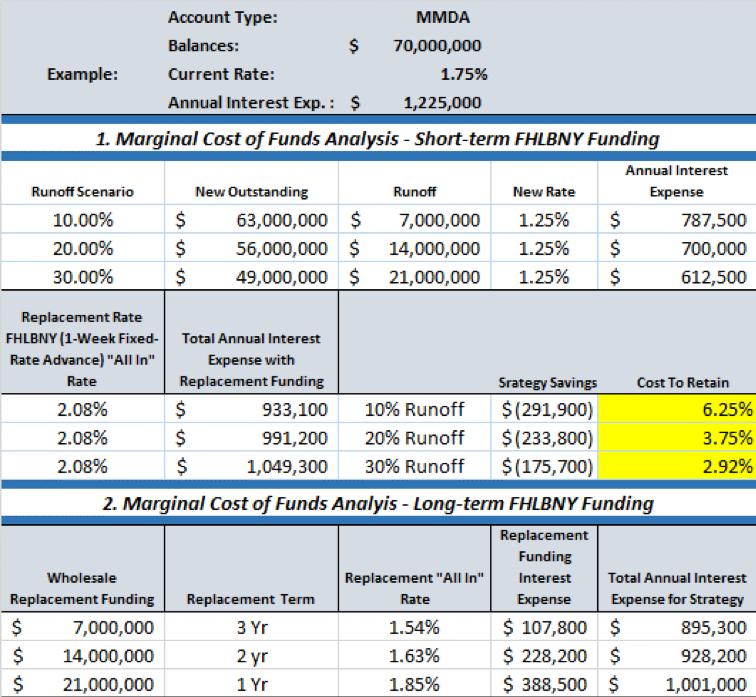

For example, let’s take a closer look at the true cost of paying a current rate of 1.75% on a $70 million money market deposit account (MMDA) portfolio, versus lowering the rate 25 bps and accepting various levels of potential runoff. Let’s consider the impact of lowering MMDA rates by 25 bps, which results in runoff of 10%, 20%, or 30%. Looking at the following example, in the first strategy, we’ve lowered the MMDA interest rate by 25 bps and funded the runoff with one-month FHLBNY Fixed-Rate Advances. As you can see, your savings is dependent on the outflow level, however, even up to 30% runoff, there will be resulting savings.

The second strategy illustrates replacing the resulting deposit runoff with long-term FHLBNY Fixed-Rate Advances. Not only would you achieve significant savings in this example, you would lengthen your liabilities and help protect your institution should you be exposed to rising rates.

When you examine the marginal cost for retaining rate sensitive deposits you may be quite surprised. Assuming that a drop in rates would result in a 10% runoff of deposits, to retain those deposits you are essentially paying a marginal rate of 6.25%, versus lowering the rate on the entire account and backfilling with FHLBNY advances (see area highlighted in yellow in following example).

The reality is that the cheapest source of marginal funds is typically in the wholesale markets, particularly now. If you’re concerned with deposit runoff, now is the time to check the elasticity of your interest-bearing deposit base since replacement funding costs are relatively low. This is not to suggest that you should abandon local market deposit generation, but rather develop a more complete understanding of the true cost of raising incremental funds in alternative markets.

Deposits Equal Customers?

It is true that deposits provide an “opportunity” to cross-sell other products and services to the underlying customer/household and, everything else being equal, should theoretically be worthy of a premium. However, it is our experience that new money attracted is often more reflective of a temporary acquaintance than it is of a customer. Little is typically done by the institution to test the cross-selling capacity of these new “customers.” We often see institutions offering long-term CD specials going out many years as a means to bring in customers for cross-selling opportunities. Using such a strategy is risky as it is uncertain at best as to whether one can indeed cross-sell to these depositors. It is potentially better to use a shorter-term, less risky approach, where a premium rate is offered for a 5- or 7-month term (an adequate time period to explore selling opportunities). More often than not, these new deposits represent above-market rate funding with an uncertain chance of renewal (with the potential of early withdrawal). It is difficult to argue that an “investment” in high-cost, deposit-generating activities without a strong action plan to cross-sell will result in enhanced franchise value (return on investment).

Lack of Spread

Facing limited local market growth opportunities, many have considered using wholesale borrowings, such as FHLBNY advances, to fund the purchase of investment securities only to conclude that the available spreads are insufficient. Senior managers usually determine the resulting after-tax spreads were below their return on assets (ROA), and therefore, quickly lose interest. For others, the perceived exposure to rising rates that would occur from an interest rate risk perspective, or “value” perspective, prevents them from taking action. For example, we’ve recently seen a $10 million dollar leverage strategy for an asset-sensitive institution using 15- and 20-year mortgage-backed securities (MBSs), yielding an average of 2.05% funded with one-month borrowings, which resulted in a 162 bps spread, pre-tax, or $162,000 annually. Another leverage strategy from a well-matched institution purchasing the same mix of MBSs was funded with equal amounts of short-term advances, 4-year advances and 5-year advances, which resulted in a 133 bps spread, pre-tax, or a $133,000 increase in net interest income. This transaction actually performs better over time as rates rise and the reinvestment of cash flow reprices higher.

Regulatory Concerns and Fears

Regardless of past experiences or grapevine “war stories,” the regulatory position is clearly stated: borrowings and brokered CDs are acceptable funding sources to the extent that they are part of an institution’s overall funding plan; a position continually reconfirmed by national regulatory agencies. In our opinion, institutions that are confident in their use of wholesale funding and can clearly document how these funding sources result in improved earnings, liquidity management, and interest rate risk management should not have concerns regarding regulatory perspectives. However, if concerns with using wholesale funding have arisen during your regulatory examinations, we would be interested to learn of your experience and delighted to share our perspective and insights for responding to concerns.

For questions regarding this article, contact Frank L. Farone, Managing Director, Darling Consulting Group at (978) 463-0400, or visit www.darlingconsulting.com.

Disclaimer: Notwithstanding any language to the contrary, nothing contained in these disclosures is intended to constitute an offer, inducement, promise, or contract of any kind. Any product descriptions and pricing may be subject to change without notice.

The content provided in these disclosures is presented as a courtesy to be used only for informational purposes and is not represented to be error free. The FHLBNY makes no representations or warranties of any kind with respect to the content contained herein, such representations and warranties being expressly disclaimed. The FHLBNY is not a financial or investment advisor.

Moreover, the FHLBNY does not represent or warrant that the content of these disclosures is accurate, complete or current for any specific or particular purpose or application. It is not intended to provide nor should anyone consider that it provides legal, accounting, tax or other advice. Such advice should only be rendered in reference to the particular facts and circumstances appropriate to each situation. The FHLBNY encourages you to contact appropriate professional(s) and consultant(s) to assess your specific needs and circumstances and to render such advice accordingly. In addition, the FHLBNY is not endorsing or recommending the use of the means or methods contained in or through these disclosures for any special or particular purpose.

It is solely your responsibility to evaluate the risks or merits of any funding or investment strategy. In no event will FHLBNY or any of its officers, directors or employees be liable for any damages — whether direct, indirect, special, general, consequential, for alleged lost profits, or otherwise – that might result from any use of or reliance on these materials.

Key Contacts

Relationship Managers:

(212) 441-6700

Member Services Desk:

(212) 441-6600 or

(800) 546-5101, option 1